Prohibitions targeted to prevent China’s exploitation of dual-use technology

On August 9, 2023, President Biden signed a historic Executive Order on Addressing United States Investments in Certain National Security Technologies and Products in Countries of Concern (the “Order”) that directs the creation of a first-ever program (the “Program”) imposing restrictions on outbound foreign investment to address the national security threat posed by certain countries of concern. The Order identifies such countries as those seeking to develop and exploit sensitive or advanced technologies and products critical for military, intelligence, surveillance, or cyber-enabled capabilities. The Order was delayed several months from its initial expected release in April 2023, but the Program tracks what was predicted in our previous client alert. While the Order gives broad guidance, the U.S. Department of the Treasury (“Treasury”) simultaneously issued a fact sheet and a more detailed Advance Notice of Proposed Rulemaking (“ANPRM”) to provide clarity about the intended scope of the Program and solicit input from the public before the Program is implemented.

The new Program will be established and administered by Treasury with input from the Department of Commerce and others. It will either require notification of, or outright prohibit, particular U.S. person investment transactions in companies conducting discrete activities in specified sectors involving entities in or subject to the jurisdiction of, or certain other entities owned by persons of, a country of concern. The Order lists the following three sectors: (1) semiconductors and microelectronics, (2) quantum information technologies, and (3) artificial intelligence systems. It identifies only the People’s Republic of China (“PRC”), including Hong Kong and Macau, as a “country of concern.” While currently focused on these technologies and geography, the Order provides flexibility for further expansion of both the specified sectors and the countries of concern; Congress has already shown significant interest in requiring such expansions.

KEY QUESTIONS

When do we have to comply with the new Program?

The Program is not yet in effect so there are no current requirements. The ANPRM simply lays out the broad contours of what Treasury is currently proposing for the Program and solicits feedback on those proposals, as well as on at least 83 included questions. The public has 45 days (until September 28, 2023) to file any comments. The ANPRM notes that draft regulations will follow at some point, which may offer another opportunity to provide public comments before the Program goes live at a yet-to-be-revealed date.1Notably, the basis of the Order’s authority is the International Emergency Economic Powers Act (“IEEPA”) (50 U.S.C. § 1701 et seq.) which requires a declared national emergency under the National Emergencies Act for the President to take action. Thus, because President Biden declared the threat from Chinese technologies to be a national emergency, Treasury could issue an Interim Final Rule after receiving ANPRM comments, which would allow the Program to go into effect immediately while also still providing for the receipt of comments and possible changes before a Final Rule is issued. In the interim period, however, it is important that investors review their funds and investment strategies to determine how the Program as currently proposed would affect them. It may also be advisable to file comments and help shape the ultimate Program.

Will the Program apply to existing investments?

The Program will not be retroactive. Although the Program requirements will apply only to those transactions made after the regulations go into effect, Treasury may request information about any transaction that was completed or agreed to after the Order went into effect (i.e., August 9, 2023), even as the rulemaking process is ongoing. It is likely that such inquiries will effectively function like the Program’s version of the CFIUS non-notified process, rooting out and possibly even enforcing against transactions that were prohibited or notifiable under the regulations. Although pre-Order transactions will not be subjected to inquiries or the new restrictions, Treasury could apply the forthcoming regulations to follow-on investments or restructuring of existing investments that are related to those pre-Order transactions, particularly if the new investment would incrementally result in an arrangement that would otherwise be within the Program’s scope.

Which investors will the Program cover?

The Program will apply to transactions by U.S. Persons, wherever located. The ANPRM defines a “U.S. Person” to include “any U.S. citizen, lawful permanent resident, entity organized under the laws of the United States or any jurisdiction within the United States, including any foreign branches of any such entity, and any person in the United States.” This definition of U.S. Person is identical to the definition Treasury uses in U.S. economic sanctions programs that are based on the President’s statutory authority under IEEPA. The regulations will likely provide examples of what sorts of scenarios are covered or not covered by this definition. For example, depending on how broadly the regulations describe “any person in the United States,” that phrase could be interpreted as even encompassing a transaction effectuated by a foreign citizen passing through U.S. airspace while flying from one foreign country to another.

For which recipients will the Program limit our investments?

The Program will apply to transactions with Covered Foreign Persons, wherever located. The ANRPM defines a “Covered Foreign Person” as “(1) a person of a country of concern that is engaged in, or a person of a country of concern that a U.S. person knows or should know will be engaged in, an identified activity with respect to a covered national security technology or product; or (2) a person whose direct or indirect subsidiaries or branches are referenced in item (1) and which, individually or in the aggregate, comprise more than 50 percent of that person’s consolidated revenue, net income, capital expenditure, or operating expenses.” The ANPRM defines “Person of a Country of Concern” as “(1) any individual that is not a U.S. citizen or lawful permanent resident of the United States and is a citizen or permanent resident of a country of concern; (2) an entity with a principal place of business in, or an entity incorporated in or otherwise organized under the laws of a country of concern; (3) the government of a country of concern, including any political subdivision, political party, agency, or instrumentality thereof, or any person owned, controlled, or directed by, or acting for or on behalf of the government of such country of concern; or (4) any entity in which a person or persons identified in items (1) through (3) holds individually or in the aggregate, directly or indirectly, an ownership interest equal to or greater than 50 percent.”

Thus, for example, the Program would govern investments not only with a company incorporated in China engaged in an identified activity with respect to a covered national security technology or product, but also with a company incorporated in the United States that is controlled by Chinese shareholders and engaged in such activity. As another example, the Program would cover investments not only with a U.S. branch of a Chinese company, but also with a U.S. company whose Chinese subsidiaries comprise more than 50 percent of the U.S. company’s revenue if the U.S. company is engaged in an identified activity with respect to a covered national security technology or product. It is expected that the regulations will add further detail to the 50 percent threshold, such as clarifying whether the aggregation of subsidiaries would be determined based solely on the branches that participate in the identified activity, or whether the identified activities of one or two branches would simply be imputed to all the branches for aggregation purposes.

What kinds of transactions will the Program cover?

The Program will apply to certain categories of Covered Transactions involving a Covered Foreign Person. For both prohibited and notifiable transactions, the ANPRM defines a “Covered Transaction” to include direct or indirect (1) acquisitions of an equity interest or a contingent equity interest; (2) provisions of debt financing where convertible to an equity interest; (3) greenfield investments that could result in establishment of a Covered Foreign Person; or (4) establishments of joint ventures, wherever located, with a Covered Foreign Person or that could result in establishment of a Covered Foreign Person. Thus, the Program would capture indirect transactions where a third party outside the scope of the Program (i.e., neither a U.S. person nor Covered Foreign Person) serves as a middleman in effectuating a transaction that would otherwise be covered if it were direct.

Will the Program exempt any transactions?

The ANPRM identifies several types of Excepted Transactions based on a “lower likelihood of concern,” borrowing heavily from the rubric used by the Committee for Foreign Investment in the United States (“CFIUS”). By carving out purely passive investments, the Program will retain its focus on preventing the intangible benefits that often accompany U.S. investments (i.e., “smart money”), such as enhanced standing and prominence, managerial assistance, access to investment and talent networks, market access, and enhanced access to additional financing. Excepted Transactions will include passive investments into publicly traded securities, index funds, mutual funds, exchange-traded funds, or similar instruments (including associated derivatives) offered by an investment company. Also exempt will be de minimis passive investments made as a limited partner (“LP”) into a venture capital fund, private equity fund, fund of funds, or other pooled investment funds, where the LP contribution is solely capital into an LP structure and the LP cannot make managerial decisions, is not responsible for any debts beyond its investment, and does not have the ability (formally or informally) to influence or participate in the fund’s or a Covered Foreign Person’s decision-making or operations. No investment will be an Excepted Transaction if it affords the U.S. person rights beyond those reasonably considered to be standard minority shareholder protections (e.g., board membership or observer rights, or any other involvement beyond the voting of shares in substantive business decisions, management, or strategy of the Covered Foreign Person).

Also included as Excepted Transactions will be the following:

- U.S. Person acquisitions from a Covered Foreign Person of an entity or asset outside of the Country of Concern where the U.S. Person is acquiring all the interests held by the Covered Foreign Person;

- Intracompany fund transfers from a U.S. parent company to a subsidiary in a Country of Concern

- Transactions made pursuant to a binding, uncalled capital commitment entered into before August 9, 2023.

Additionally, while not Excepted Transactions, the following activities will not be covered by the Program so long as they are not meant to evade the restrictions and are not otherwise a Covered Transaction: university-to-university research collaborations; contractual arrangements or procurement of material inputs (i.e., raw materials); intellectual property licensing arrangements; bank lending or the processing, clearing, or sending of payments by a bank; underwriting services; debt rating services; prime brokerage; global custody; equity research or analysis; or other services secondary to a transaction.

Which investments will be prohibited, and which will be notifiable under the Program?

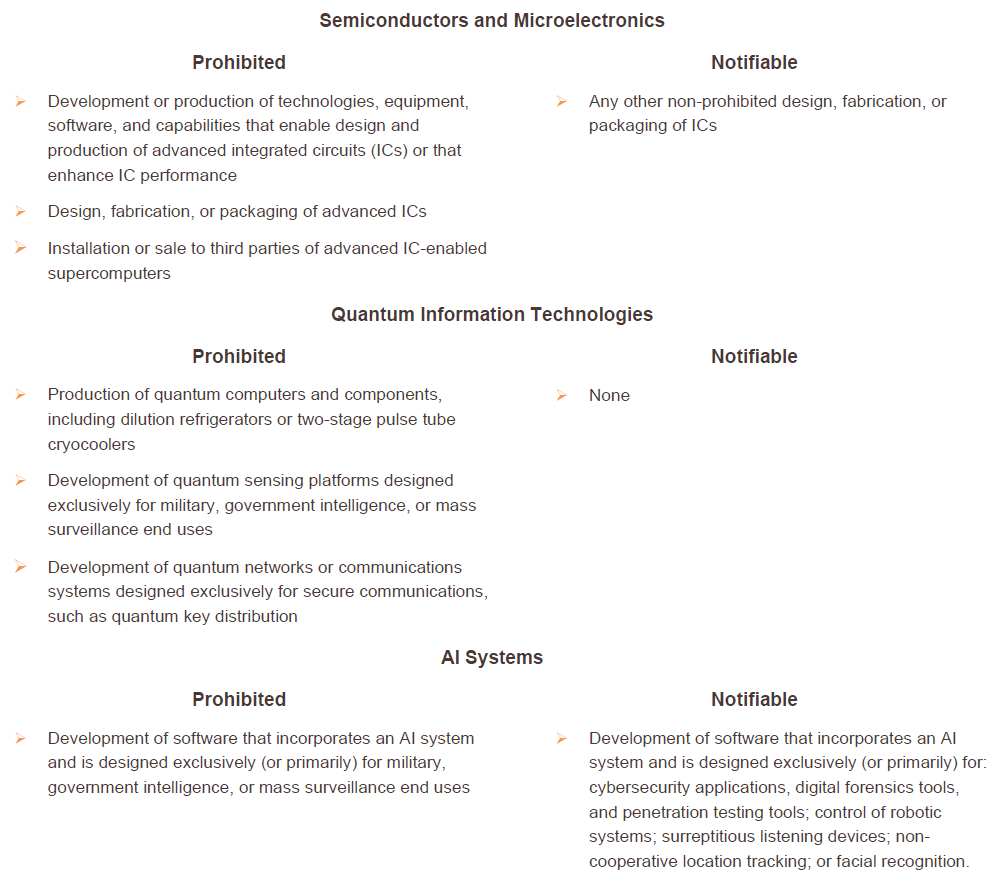

Whether an investment will be prohibited or notifiable depends on the specified type of national security technology or product involved within the three designated sectors of semiconductors and microelectronics, quantum information technologies, and artificial intelligence (“AI”) systems. The ANPRM categorizes the first sector by feature and performance criteria and defines the other two sectors as follows: Quantum computers are those that perform computations harnessing the collective properties of quantum states, such as superposition, interference, or entanglement; AI is an engineered or machine-based system that can, for a given set of objectives, generate outputs such as predictions, recommendations, or decisions influencing real or virtual environments, and that is designed to operate with varying levels of autonomy. Further details are expected in the regulations, but the current breakdown of prohibited and notifiable activities by sector is as follows:

How will the Program be enforced?

First, it is important to note that the Program will not entail a case-by-case review of transactions (i.e., a “Reverse CFIUS”) and instead will place the compliance burden upon investors, who will have to determine whether a transaction is prohibited, notifiable, or otherwise permissible without notification. Thus, the regulations will need to be very clear and detailed so that transaction parties will understand the guardrails and take action to comply. Experienced counsel will no doubt be extraordinarily helpful in assisting transaction parties through this complex analysis.

Second, the Program will pursue actions taken to evade the regulations or conspiracies to violate the regulations. For example, the Program also will prohibit U.S. Persons from knowingly directing transactions that would be prohibited if engaged in by a U.S. Person. In other words, an investor would violate the regulations if the investor orders, decides, approves, or otherwise causes the prohibited action and had actual knowledge, or should have known, about the conduct, the circumstance, or the result of the prohibited action. Thus, if a U.S. Person General Partner takes any of these actions with respect to a foreign fund that makes a prohibited investment, Treasury would find a violation. Moreover, any U.S. Persons who are senior managers at that fund and act on that General Partner’s direction are also committing a violation. A violation would also be found where several U.S. Person venture partners launch a foreign fund to make prohibited investments.

Third, the Program will place an affirmative obligation on U.S. Persons who control (i.e., directly or indirectly own a 50 percent or greater interest) foreign entities to take all reasonable steps to prohibit and prevent, or to provide the notification for, any transactions by those entities that would be prohibited or notifiable if engaged in by a U.S. Person. In considering whether “all reasonable steps” were taken, Treasury will consider factors such as (1) relevant binding agreements between a U.S. person and the relevant controlled foreign entity or entities; (2) relevant internal policies, procedures, or guidelines that are periodically reviewed internally; (3) implementation of periodic training and internal reporting requirements; (4) implementation of effective internal controls; (v) a testing and auditing function; and (5) the exercise of governance or shareholder rights, where applicable.

Finally, Treasury will have the authority to investigate violations and pursue civil penalties up to the maximum value allowed under IEEPA, which is the greater of $356,579 or twice the value of the transaction, which is notably double the maximum penalty amount that CFIUS can assess. Penalties would be assessed for making material misstatements or omissions in submissions to Treasury, conducting prohibited transactions, and failing to notify a transaction as required. Importantly, the amount can be assessed for each violation, meaning that if Treasury finds multiple violations related to a given transaction (e.g., an initial failure to file followed by a misstatement in a filing), it could assess double the transaction value for each of those violations. The Order also authorizes Treasury to refer potential criminal violations of the Order or resulting regulations to the Attorney General for criminal prosecution.

How do we file a notification and what kind of information will the Program require?

Required notifications will need to be filed through the electronic Treasury portal no later than 30 days after the closing of Covered Transactions. The filed information will be protected under confidentiality provisions similar to those used by CFIUS. The regulations are expected to expound on the information to be included in a filing, but filings will certainly include detailed information about the transaction entities, including the Covered Foreign Person; an explanation of the nature of the transaction; a description of the basis for determining the investment was a Covered Transaction, including the technology, end-users, and any rights afforded to the U.S. Person; and any documents related to the transaction. Although the ANPRM notes that the Program would not establish a case-by-case analysis, there will almost certainly be a requirement for the transaction parties to answer questions.

NEXT STEPS

Companies should not merely wait for the regulations to be released. First, if your company has questions or comments on the proposed Program, it should submit comments by the 45-day deadline so that it can shape the regulations, particularly given the ANPRM’s warning that Treasury may expand or deviate from the proposed approaches. Experienced counsel can be helpful in drafting and filing those comments on behalf of clients.

Second, for both existing investments and any investments not yet made, your company should be viewing new investments, follow-on investments, and future capital calls through the lens of the proposed Program likely to be in place soon to determine the level of possible exposure risk. Many aspects of the ANPRM reflect a borrowing from CFIUS provisions. Although a case-by-case regime may be lacking—at least initially—much of the new Program rhymes with CFIUS, which is hardly surprising since the new Program will be overseen by Treasury’s Office of Investment Security, which also chairs CFIUS. Thus, CFIUS counsel with experience inside that office may be able to provide valuable insight to companies conducting these strategic analyses and seeking to put new compliance measures into place.

Third, companies should keep an eye out for future expansions in the United States and abroad. For example, there has been recent Congressional interest in such expansions to China’s biotechnology and energy sectors, hypersonic technology, satellite-based communications, and networked laser scanning systems, as well as including Russia, Iran, and North Korea as “countries of concern.” Additionally, the United States has been coordinating its approach with allies and partners for quite a while, resulting in many countries expressing a willingness to implement complementary programs. While expansions would further complicate compliance, increased restrictions could also prompt China to retaliate against companies with a China presence. Engaging counsel with a strong Federal affairs practice and international presence may be useful to clients as these expansions take shape.

King & Spalding has a global footprint, substantial industry experience, and deep bench of former trade and national security government officials, including a former U.S. Department of Treasury official who recently helped lead the Office of Investment Security, which chairs CFIUS and will oversee the new outbound investment screening regime. King & Spalding is uniquely positioned to guide companies through preparing for the historic implementation of this new regulatory program.