On October 10, 2023, the Securities and Exchange Commission (the “Commission”) adopted final rules amending the beneficial ownership reporting requirements established by the Commission under Sections 13(d) and 13(g) of the Securities Exchange Act of 1934 (the “Exchange Act”).1The fact sheet for the final rules can be found here and the adopting release for the final rules can be found here (the “Adopting Release”). The intent behind these amendments is to improve transparency in investor beneficial ownership reporting and modernize the beneficial ownership reporting regime, the basic framework of which was put in place more than 50 years ago.

The final amendments contain significant changes from the amendments initially proposed by the Commission in February 2022 as the Commission elected not to adopt several of its more impactful (and more hotly contested) proposals. In particular, the Commission elected not to adopt proposed rules that would (i) deem the holder of a cash-settled derivative to beneficially own the underlying reference security in certain circumstances and (ii) potentially alter the dynamics of when two or more investors constitute a “group” for purposes of reporting beneficial ownership. The Commission instead issued guidance concurrently with issuing the final rules that addresses the treatment of these omitted proposals under existing Commission rules. This guidance is substantially consistent with existing law and market practice, however, so it will likely have little impact on investor behavior.

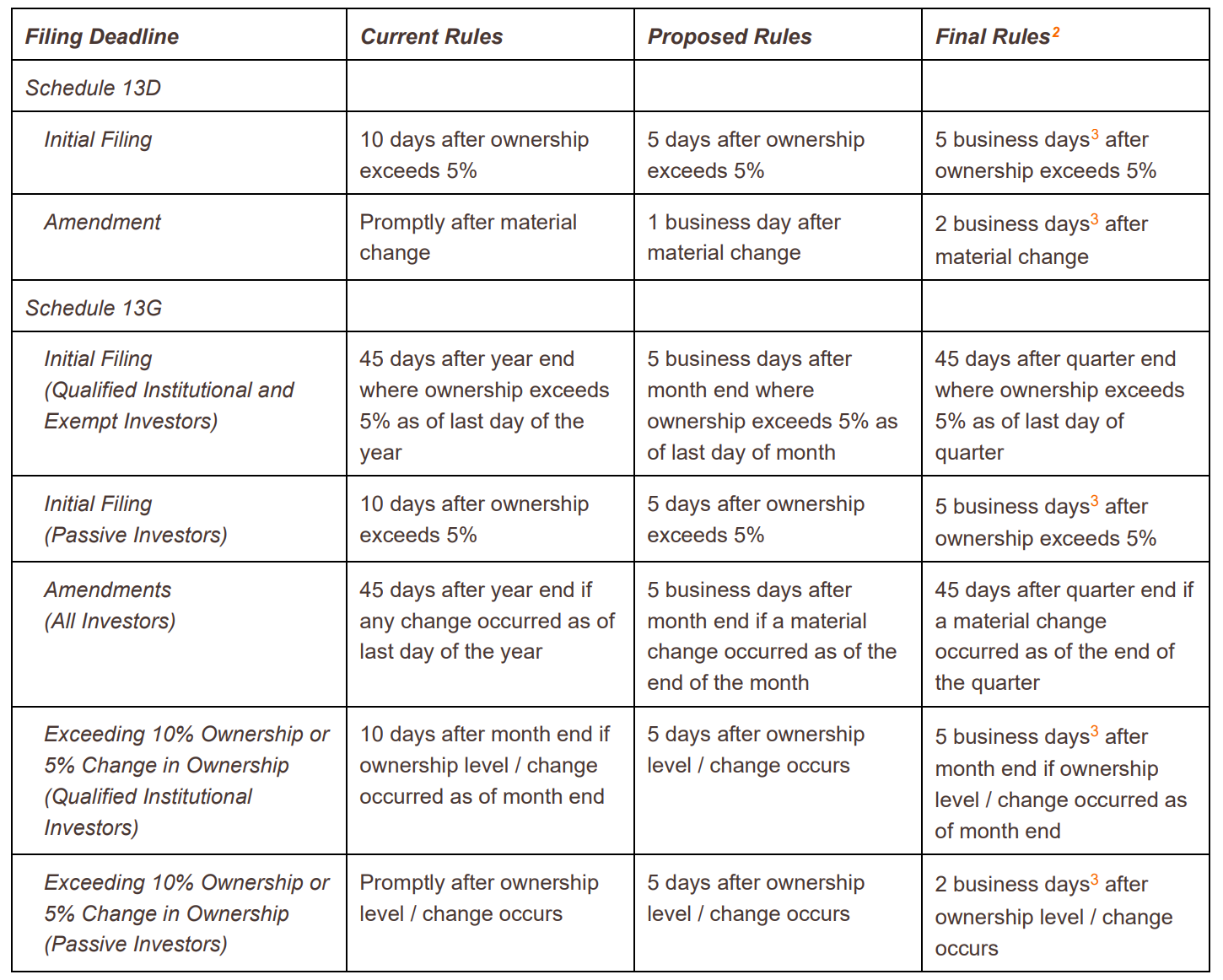

Revised Schedule 13D and Schedule 13G Filing Deadlines

In light of, among other things, technological improvements in the dissemination and consumption of information by market participants, the Commission amended the beneficial ownership reporting rules to shorten the relevant deadlines by which an investor must file or amend a Schedule 13D or 13G. While these deadlines shorten the relevant reporting deadlines compared to current rules, each final deadline backtracks slightly from the deadlines initially proposed by the Commission. The table below details the current, proposed and final amended filing deadlines for each class of investor and each submission type.

Filing Deadline Comparison Table

2The day after the date of acquisition is counted as day one for purposes of calculating relevant business day deadlines. 3The final rules define a business day as the period from 12:00 a.m. to 11:59 p.m., Eastern time, on any day other than a Saturday, Sunday or federal holiday. Despite this definition, Schedule 13D and G filings are subject to Regulation S-T which, as revised by the final rules, specifies a filing cutoff time period of 10:00 p.m., Eastern time, for Schedule 13D and G filings made through EDGAR. As a result, despite the new business day definition, the effective end of the business day is 10:00 p.m. Eastern time for filings made through EDGAR.

2The day after the date of acquisition is counted as day one for purposes of calculating relevant business day deadlines. 3The final rules define a business day as the period from 12:00 a.m. to 11:59 p.m., Eastern time, on any day other than a Saturday, Sunday or federal holiday. Despite this definition, Schedule 13D and G filings are subject to Regulation S-T which, as revised by the final rules, specifies a filing cutoff time period of 10:00 p.m., Eastern time, for Schedule 13D and G filings made through EDGAR. As a result, despite the new business day definition, the effective end of the business day is 10:00 p.m. Eastern time for filings made through EDGAR.

Other Rule Amendments

The final rules also make the following revisions to existing Schedule 13D and 13G disclosure requirements:

- Amendments to Required Schedule 13D Exhibits. The final rules amend Item 6 of Schedule 13D to clarify that an investor filing on Schedule 13D (i) must disclose its interest in all derivative securities (including cash-settled derivatives) that use the issuer’s equity securities as a reference security and (ii) does not need to disclose any instruments or arrangements other than those specifically listed in Item 6.

- Standard for Schedule 13G Amendments. In addition to amending the timeline for filing an amendment to a Schedule 13G as discussed above, the final rules revise the standard for amending a Schedule 13G from “any change” to “any material change” in the information reported. While this initially seems like an impactful change, the Commission noted that the final rules are consistent with the Commission’s existing view that “there is a materiality standard inherent in the provisions governing Schedule 13G filings.”4Adopting Release at 78-79. However, the Commission also noted, consistent with existing guidance, that any disclosure in a Schedule 13G is “effectively material” as a result of the “infrequency of the reports and comparatively minimal statements required to be made” as part of a Schedule 13G. See id. As a result, this change should not substantively affect the standard for triggering an amendment to a Schedule 13G.

- Machine Readable Filings. The final rules require that all Schedule 13D and 13G filings (other than exhibits) be made using structured, machine-readable data language (e., an XML-based format).

Guidance Concerning Treatment of Cash Settled Derivatives

In the face of significant investor pushback, the Commission did not adopt its initial proposal to Rule 13d-3 to deem holders of cash-settled derivatives to be the beneficial owners of the underlying reference securities when those derivatives are held with the purpose or effect of changing or influencing the control of the issuer (or in connection with or as a participant in any transaction having such purpose or effect). The Commission instead issued guidance that an investor may beneficially own reference securities underlying a cash-settled derivative where:5Adopting Release at 114-115. This new guidance is generally consistent with the Commission’s guidance concerning beneficial ownership of reference securities underlying securities based swaps.

- The holder of the derivative has voting or dispositive power over the reference securities;

- The derivative is “acquired with the purpose or effect of divesting its holder of beneficial ownership of the reference [securities] or preventing the vesting of that beneficial ownership as part of a plan or scheme to evade” beneficial ownership reporting; or

- The holder has the right to acquire beneficial ownership of the reference securities within 60 days or acquires the right to acquire beneficial ownership of the reference securities in connection with a transaction having the purpose or effect of changing or influencing control of the issuer, even if such right originates from a nominally cash-settled derivative or an understanding in connection with such a derivative.

Guidance Concerning Determinations of Group Status

The Commission also elected not to adopt substantially all of its amendments to Rule 13d-5, including proposed amendments that would (i) remove references that persons must “agree” to act as a group for a group to be formed and (ii) deem a group to exist where one investor tips another investor about its obligation to file an upcoming Schedule 13D with the intent that the second investor purchase securities. Instead, the Commission reaffirmed its position that the determination of whether investors “agree” to act as a group is a fact-specific determination and does not require a written or other formal arrangement between investors. The Commission also provided guidance consisting of several examples of conduct that it would or would not consider to be indicative of group status among investors. These examples include the following:

- A group is generally not formed in the following instances:

- Two or more shareholders communicate with each other regarding the long-term performance of an issuer, changes in issuer practices, submission or support of non-binding shareholder proposals, a joint engagement strategy (not control related), or a “vote no” campaign in an uncontested election, in each case without taking any other actions.

- Two or more shareholders engage in discussions with an issuer’s management without taking any other actions.

- Two or more shareholders jointly make recommendations to an issuer regarding the structure and composition of its board of directors, provided that (1) no discussion of individual directors or board expansion occurs and (2) no commitments are made among the shareholders regarding the withholding of votes, or voting against, management director candidates.

- Two or more shareholders jointly submit a non-binding shareholder proposal pursuant to Exchange Act Rule 14a-8.

- A conversation, email, phone contact, or meetings between a shareholder and an activist investor that is seeking support for its proposals to an issuer’s board or management, without more (such as consenting or committing to a course of action).

- Announcement of an intent to vote for another investor’s director nominees, without further action.

- A group may be formed where an investor required to file a Schedule 13D intentionally communicates to another market participant that such a filing will be made (to the extent that information is not yet public) with the purpose of causing the market participant to make purchases in the same covered class of securities (and the purchases are made).6Note that the new guidance requires the market participant informed of the upcoming Schedule 13D filing to purchase securities, a requirement that was not stated on the face of the proposed rule.

In practice, any determination of group status is a highly fact-specific inquiry, and these examples are not an exhaustive list of the actions and situations that may be taken with or without resulting in a group being formed.

Compliance Deadlines

The final amendments will become effective 90 days after publication in the Federal Register. Compliance with the revised Schedule 13G filing deadlines will be required beginning on September 30, 2024. Compliance with the structured data requirement for Schedules 13D and 13G will be required on December 18, 2024.