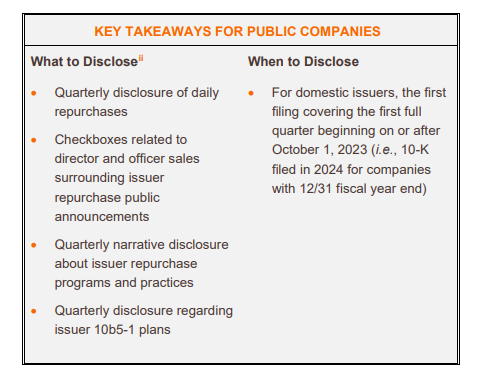

On May 3, 2023, the U.S. Securities and Exchange Commission (the “Commission”) adopted amendments to its rules regarding share repurchase disclosures (the “Final Rules”) in an effort to enhance transparency and accountability.1The fact sheet for the Final Rules can be found here and the adopting release for the Final Rules can be found here.

2Specifically, the Commission amended Item 703 (Purchases of equity securities by the issuer and affiliated purchasers), Item 601 (Exhibits), and added Item 408(d) (Insider trading arrangements and policies) of Regulation S-K. For Foreign Private Issuers (“FPIs”), the Final Rules added Rule 13a-21, amended Item 16E of Form 20-F, and added Form F-SR. For Listed Closed-End Funds, the Final Rules added Form N-CSR. The Final Rules do not provide scaled disclosure for smaller reporting companies.

2Specifically, the Commission amended Item 703 (Purchases of equity securities by the issuer and affiliated purchasers), Item 601 (Exhibits), and added Item 408(d) (Insider trading arrangements and policies) of Regulation S-K. For Foreign Private Issuers (“FPIs”), the Final Rules added Rule 13a-21, amended Item 16E of Form 20-F, and added Form F-SR. For Listed Closed-End Funds, the Final Rules added Form N-CSR. The Final Rules do not provide scaled disclosure for smaller reporting companies.

In an important change from the proposed rules, the Commission is not requiring a next business day filing obligation for share repurchases in the Final Rules.

Also of note, the Final Rules confirm that issuers will not be subject to a mandatory “cooling-off” period for issuer 10b5-1 plans, which had remained an open question following the adopting release for the new rules regarding director and officer 10b5-1 plans released in December 2022.3The adopting release for the new rules regarding insider trading arrangements and related disclosures, adopted in December 2022, can be found here.

Summary of the Final Rules

Quantitative Disclosure

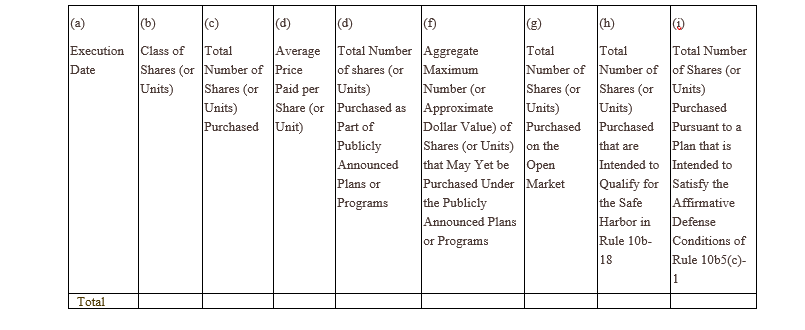

- New Exhibit for 10-Qs/10-Ks; No Next Day Reporting - While the Final Rules still require the disclosure of daily repurchase data, the originally proposed next business day reporting on Form SR was not adopted. Instead, issuers that file on domestic forms must disclose daily quantitative repurchase data at the end of every quarter in an exhibit filed4In a departure from the proposed amendments, the Final Rules treat the exhibit disclosure as “filed” material, as opposed to information “furnished” to the Commission. with their Form 10-Q and Form 10-K (for the fourth fiscal quarter).5The disclosure amendments apply to issuers with classes of equity securities registered pursuant to Section 12 of the Exchange Act. “Issuers,” for purposes of the adopting release, includes affiliated purchasers and any person acting on behalf of the issuer or an affiliated purchaser. Listed Closed-End Funds must disclose such data in their annual and semi-annual reports on Form N-CSR. FPIs must disclose such data at the end of every quarter in the new Form F-SR, which will be due 45 days after the end of the FPI’s fiscal quarter. This new requirement will replace the current requirement under Item 703 of Regulation S-K to disclose aggregate monthly repurchases.

- Disclosure Requirements in Exhibit - The following table will be required to be filed as an exhibit to Form 10-Qs and 10-Ks (for issuers that file on domestic forms) disclosing daily repurchases by issuers and affiliated purchasers. FPIs will be required to file similar tabular disclosure in a new Form F-SR within 45 days after the end of a fiscal quarter:

Issuers will also be required to include a footnote to the table above disclosing the date any 10b5-1 plan was adopted or terminated.

- Required Checkbox - Issuers are required to indicate by checkbox above the tabular disclosure whether or not Section 16 officers (certain D&Os in the case of FPIs) purchased or sold securities subject to a share repurchase plan within four business days before or after the announcement of the plan or program, or the announcement of an increase of an existing share repurchase plan or program (as opposed to ten business days as proposed).

Narrative Disclosure in 10-Qs/10-Ks

The Final Rules require an issuer to disclose the following in narrative format in 10-Qs and 10-Ks:6The following requirements are included in Regulation S-K Item 703 for filers using domestic forms (10-Q/10-K) and in Form 20-F for FPIs not filing on domestic forms.

- Objectives/Rationales - The objectives or rationales for each repurchase plan or program and process or criteria used to determine the amount of repurchases, the number and nature of transactions of securities purchased other than through publicly announced plans or programs, and certain other information regarding the conduct of these plans or programs.7Additionally, for publicly announced plans, issuers must disclose the date each plan or program was announced, the dollar or share amount approved, the expiration date for such plans or program, each plan or program that expired during the period covered by the exhibit table, and each plan or program the issuer has determined to terminate prior to expiration, or under which it intends to make no further purchases.

- Policies and Procedures for D&Os - Any policies and procedures relating to purchases and sales of its securities by its officers and directors during a repurchase program, including any restriction on such transactions.

Issuer 10b5-1 Plan Information

As a complement to the repurchase disclosures, new Item 408(d) will require issuers to disclose the following in Form 10-Qs and 10-Ks (for the fourth fiscal quarter):8Notably, a cross reference to Item 703 disclosure can meet this requirement if all required information is included.

- Whether, during its most recently completed fiscal quarter, the issuer adopted or terminated a contract, instruction, or written plan to purchase or sell its securities intended to satisfy the affirmative defense conditions of Rule 10b5-1(c).9However, in a change from the proposed Item 408(d), issuers will not be required to disclose information about the adoption or termination of any trading arrangement for the purchase or sale of securities of the issuer that meets the requirements of a “non-Rule 10b5-1 trading arrangement” as defined in Item 408(c).

- Material terms of the contract, instruction, or written plan, including date, duration and aggregate securities to be purchased or sold. Consistent with the new disclosure rules regarding director and officer 10b5-1 plans, the rules do not require issuers to disclose pricing terms.

Analysis and Takeaways

While the Final Rules represent a scaled-back version of the initial proposal, the new disclosure obligations will require meaningful preparation. To be prepared, we recommend the following:

- Establish controls and procedures to capture and report the required daily repurchase data. Creating a set of new controls and procedures to accurately track and report the required information on a daily basis will require coordination among brokers, management, financial reporting and legal teams. As noted, domestic issuers are required to include the tabular disclosure set forth in the table above in 10-Qs and 10-Ks (and tag the disclosure using Inline XBRL) starting with the first filing that covers the first full fiscal quarter that begins on or after October 1, 2023. For calendar year-end domestic issuers, that means this will be required (covering Q4) in the 10-K for the year ending December 31, 2023 (i.e., this year). In a change from the proposed rule, this data (which will be presented in a new exhibit, in lieu of the existing repurchase table required under current Item 703) will be filed, not furnished, opening the door to potential liability, including Section 11 claims.

- Consider your narrative around insider trades (if any). Companies will be required to check a box above the table to indicate if any purchases or sales by Section 16 officers or directors were made within four business days before or after the company’s announcement of a new or increased repurchase plan. This does not provide any information that is not already available through Section 16 filings, but companies should consider providing additional disclosure (in the form of a footnote to the table or other narrative disclosure) to add context to trades (e.g., the trades were made under long-established 10b5-1 plans or were automatic sales to fund tax withholding on vesting). We recommend syncing up any incremental disclosure here with voluntary footnotes on Form 4s.

- Consider how to narrate the Company’s “objectives or rationales” for repurchase plans, and the “criteria used to determine the amount of repurchases.” In discussing the need for this new required disclosure, the adopting release reiterates that the Commission is not looking for boilerplate language. However, crafting this disclosure in a way that is anything other than boilerplate will require artful consideration each quarter, including in respect of board discussions. Thematically, the adopting release makes it clear that the Commission is focused on helping investors identify repurchases in which efforts to affect compensation or accounting measures may have played a role. We recommend keeping this concern, which is pervasive in the adopting release, front of mind when establishing polices (see below) and drafting responsive disclosures.

- Be mindful of the timing of 10b5-1 plans. As noted above, the Commission is not implementing a mandatory “cooling-off” period for issuer 10b5-1 plans. While there is no technical prohibition on issuers entering a 10b5-1 plan that begins trading immediately (assuming the other conditions of Rule 10b5-1 are met), issuers will be required to disclose, among other things, the date of adoption of 10b5-1 plans and the dates of the corresponding trades. Accordingly, we recommend that companies are mindful of when trades will occur relative to the adoption of the plan, particularly as it relates to the disclosed “objectives or rationales” of the repurchase plan. Concerns regarding plan timing increase around quarter end and material events.

- Evaluate policies and procedures relating to trading by officers and directors during a repurchase program. The Final Rules require disclosure of any policies and procedures relating to purchases and sales of the issuer’s securities by its officers and directors during a repurchase program, including any restrictions on such transactions. In our experience, where policies and procedures of this nature exist, they are often informal and often ad hoc. While the adopting release is clear that this is a disclosure obligation and not a requirement for an issuer to have, adopt or change any such policies and procedures, whether the disclosure obligation will effectively become a normative requirement will remain to be seen.10This requirement is incremental to the requirement, adopted in December 2022, to disclose whether the company has adopted insider trading policies governing trades by insiders, or the company itself. These disclosures around (and the accompanying requirement to file) insider trading policies will not be required for calendar year end domestic issuers until the Form 10-K for the year ending December 31, 2024. However, due to the potential overlapping subject matter, it would be prudent to consider both new sets of disclosure requirements together.

Timeline for Compliance

- Most Issuers - Narrative disclosure and exhibit to Form 10-K and 10-Q starting with the first filing covering the first full quarter beginning on or after October 1, 2023 (10-K for FY 23, filed in 2024).

- FPIs - New Form F-SR starting with first Form F-SR covering the first full fiscal quarter beginning on or after April 1, 2024 (Q2 24) due 45 days after quarter end. Narrative disclosure starting in the first Form 20-F filed after the first Form F-SR has been filed.

- Listed Closed-End Funds - First Form N-CSR for the first 6-month period beginning on or after January 1, 2024.