Proposed rules are moderately scaled-back in final version; Scope 1 and 2 are required if material; Scope 3 is out; compliance will still be burdensome

On March 6, 2024, by a split vote of 3-2, the U.S. Securities and Exchange Commission (the “Commission”) adopted final rules under the Securities Act of 1933 (the “Securities Act”) and Securities Exchange Act of 1934 (the “Exchange Act”) that require registrants to provide certain climate-related information in their registration statements and periodic reports. While the final rules represent a moderately scaled-back version of the proposed rules issued on March 21, 2022 and discussed in our prior client alert, compliance will still be burdensome in both time and expense.

HIGHLIGHTS:

- Scope 1 and 2 greenhouse gas (“GHG”) disclosures are required, if material, for large accelerated and accelerated filers; Scope 3 has been excluded

- Requirements remain for GHG assurance (on Scope 1 and 2) and disclosure of material climate related risks (plus board oversight and management actions regarding these risks)

- Disclosure is required on material climate-related targets and goals

- Disclosure of effects of severe weather events and other natural conditions including, for example, costs and losses, required in note to financial statements at very low thresholds

- No express reciprocity or preemption of cross-border or state law regimes (e.g. California)

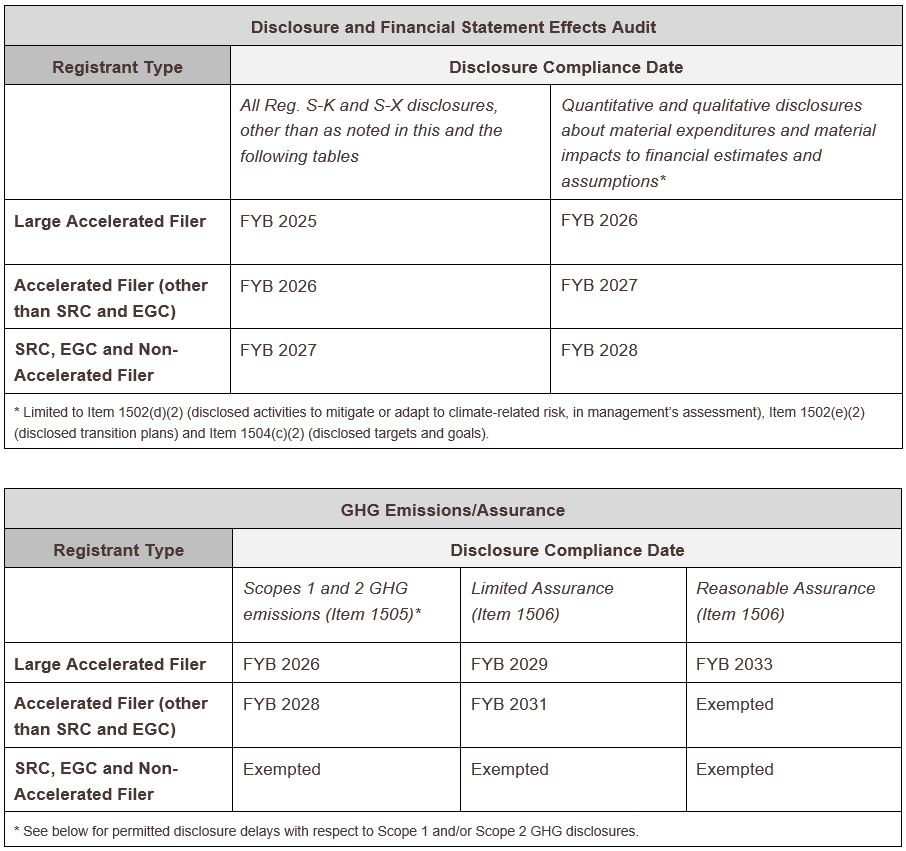

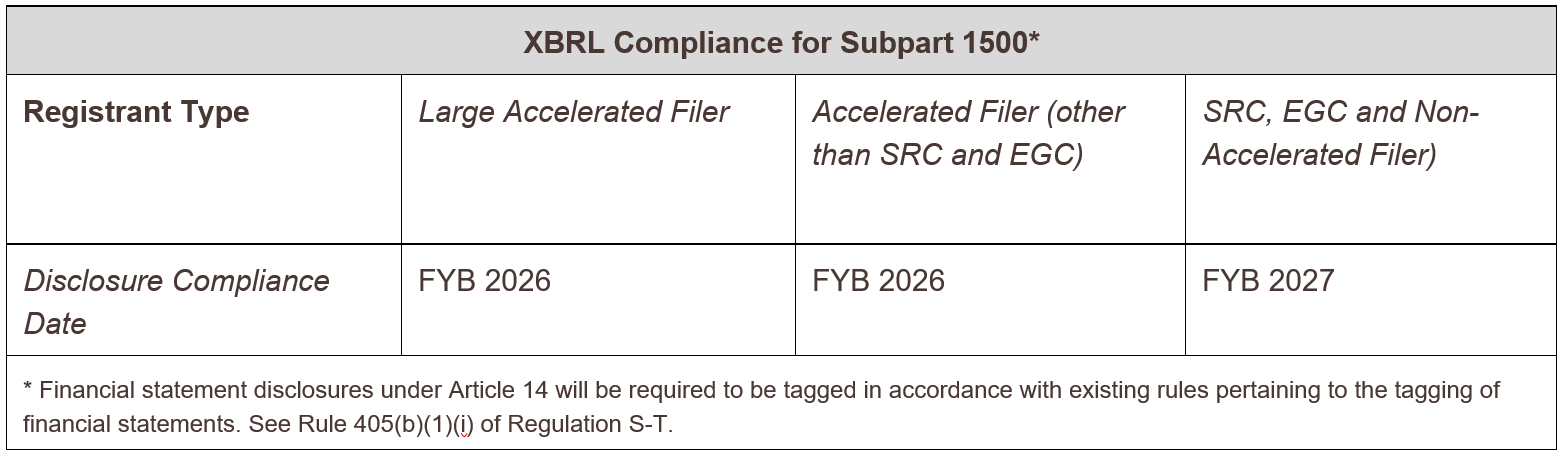

TIMELINES FOR COMPLIANCE

The phased-in compliance periods for the final rules are included in the tables and commentary below. The Commission’s references to FYB below refer to “fiscal year beginning”, which means the disclosure will need to capture the noted FYB year. Accordingly, companies with calendar fiscal year-ends will generally first include the required disclosures in their annual report filed in the spring of the following calendar year (i.e. FYB 2025 requires inclusion in the annual report filed in 2026). There are however, specific rules for registration statements and some ability to delay Scopes 1 and/or Scope 2 GHG emissions disclosures.

The final rules also include an accommodation that allows Scope 1 and/or Scope 2 emissions disclosure, if required, to be filed on a delayed basis as follows:

- Domestic registrant: May file emissions disclosures in (1) its annual report on Form 10-K, (2) its Form 10-Q for the second fiscal quarter in the fiscal year following the year to which the GHG data relates or (3) an amendment to its previously filed Form 10-K by the deadline of the Q2 Form 10-Q;

- Foreign private issuer: May file emissions disclosures in an amendment to its annual report on Form 20 F, which shall be due no later than 225 days after the end of the fiscal year to which the GHG emissions disclosure relates; and

- Registration statements: In Exchange Act or Securities Act registration statements, will include emissions disclosures as of the most recently completed fiscal year that is at least 225 days prior to the date of effectiveness of the registration statement.

The final rules do not include a requirement to disclose material changes in subsequent Form 10-Q or Form 6-K filings.

DISCLOSURES REQUIRED BY THE FINAL RULES

The final rules require a registrant to disclose:

Climate Related Risk Information

- Risk identification: Climate-related risks that have had or are reasonably likely to have a material impact on the registrant’s business strategy, results of operations or financial condition;

- Impact of risks: The actual and potential material impacts of any identified climate-related risks on the registrant’s strategy, business model and outlook;

- Mitigation and expenditures regarding risks:

- Qualitative and quantitative disclosure: If, as part of its strategy, a registrant has undertaken activities to mitigate or adapt to a material climate-related risk, a quantitative and qualitative description of material expenditures incurred and material impacts on financial estimates and assumptions that directly result from such mitigation or adaptation activities;

- Specifics on plans and pricing: Specified disclosures regarding a registrant’s activities, if any, to mitigate or adapt to a material climate-related risk including the use, if any, of transition plans, scenario analysis or internal carbon prices;

Oversight and Process

- Board oversight: Any oversight by the board of directors of climate-related risks and any role by management in assessing and managing the registrant’s material climate-related risks;

- Process for risk management and identification: Any processes the registrant has for identifying, assessing, and managing material climate-related risks and, if the registrant is managing those risks, whether and how any such processes are integrated into the registrant’s overall risk management system or processes;

- Goals and targets, with materiality qualifier: Information about a registrant’s climate-related targets or goals, if any, that have materially affected or are reasonably likely to materially affect the registrant’s business, results of operations or financial condition. Disclosures would include material expenditures and material impacts on financial estimates and assumptions as a direct result of the target or goal or actions taken to make progress toward meeting such target or goal;

GHG Emissions Information

- Scope 1 and 2: For large accelerated filers and accelerated filers that are not otherwise exempted, information about material Scope 1 emissions and/or Scope 2 emissions;

- Assurance: For those required to disclose Scope 1 and/or Scope 2 emissions, an assurance report at the limited assurance level, which, for a large accelerated filer, following an additional transition period, will be required at the reasonable assurance level;

- Required disclosure on change in or disagreement with attestation provider: The final rules require that a company disclose certain information when a company’s GHG emissions attestation provider resigns, declines to stand for re-appointment or is dismissed or there were disagreements with that provider;

Financial Statement Information

- Costs of severe weather and natural conditions with 1% and de minimis thresholds: The capitalized costs, expenditures expensed, charges and losses incurred as a result of severe weather events and other natural conditions, such as hurricanes, tornadoes, flooding, drought, wildfires, extreme temperatures and sea level rise, subject to applicable one percent and de minimis disclosure thresholds, disclosed in a note to the financial statements;

- Carbon offset and REC costs: The capitalized costs, expenditures expensed and losses related to carbon offsets and renewable energy credits or certificates (“RECs”) if used as a material component of a registrant’s plans to achieve its disclosed climate-related targets or goals, disclosed in a note to the financial statements;

- Qualitative description of impact of severe weather and natural conditions to climate targets, estimates and assumptions: If the estimates and assumptions a registrant uses to produce the financial statements were materially impacted by risks and uncertainties associated with severe weather events and other natural conditions or any disclosed climate-related targets or transition plans, a qualitative description of how the development of such estimates and assumptions was impacted, must be disclosed in a note to the financial statements;

Limited Safe Harbors

- Limited safe harbor: The final rules include a limited safe harbor from private liability for forward-looking climate-related disclosures (excluding historical facts) pertaining to transition plans, scenario analysis, the use of an internal carbon price and targets and goals. These specific disclosures will be considered forward-looking statements for purposes of Private Securities Litigation Reform Act protections; and

- SRC and EGC scaled disclosure: The final rules provide an exemption from the GHG emissions disclosure and attestation requirements for SRCs and EGCs.

KEY TAKEAWAYS AND PRACTICAL CONSIDERATIONS

In the two years that have passed since the release of the proposed rules in March 2022, companies have taken a wide range of approaches to climate-related disclosures in SEC filings and voluntary reports. In addition, laws mandating climate disclosures have become effective in the United States and beyond, adding complexity to the landscape. Preparation to report under the final rules will require significant efforts and consideration of factors beyond the black letter of the final rules. As companies begin to prepare, here are some preliminary practical considerations:

- Consider materiality of Scope 1 and 2: Consider carefully the company’s position on materiality of Scope 1 and Scope 2 GHG disclosures. A seemingly significant change between the proposed rules and final rules is the inclusion of a materiality qualifier on GHG emissions. Any determination that Scope 1 and/or 2 emissions are not material, if questioned, will be viewed in hindsight, and such determination should be undertaken and documented with legal counsel and accounting firm involvement. More generally, many of the new disclosure requirements are qualified by materiality and will require complex analysis of materiality in the context of climate risk.

- Revisit disclosure controls and procedures and ICFR: Examine and revise disclosure controls and procedures surrounding GHG emissions and other areas of mandated disclosure (including risks and impact of weather events and natural conditions). Internal controls over financial reporting are also implicated by the new Regulation S-X requirements and should be evaluated, as necessary. Because components of the final rules require both a materiality determination and measurement of financial impact regarding severe weather events and other natural conditions, as well as climate targets, proactively examine internal data collection and reporting processes so as to be positioned to make these determinations accurately and effectively (with an eye towards the phased-in attestation requirements).

- Begin discussions with attestation providers: Though the runway is long, begin to engage with potential providers of GHG attestations that meet the expertise and independence requirements of the final rules. Understanding their capabilities, costs, requirements and timelines will be critical. Notably, a resignation or dismissal of the provider and certain disagreements with them will require disclosure.

- Build a calendar and checklist: Create or update a filing calendar or gantt chart that incorporates the necessary timelines and tasks required to meet the requirements of the final rules and takes into consideration where the final rules overlap with, and diverge from, other mandatory and voluntary reporting.

- Follow legal challenges: In the wake of the successful challenge of the Share Repurchase Disclosure Modernization rules and the 5th Circuit’s vacating those final rules, litigation challenging the final rules has already been filed (despite the scaling back from the proposed rules). West Virginia v. EPA and the recent cases at the Supreme Court examining Chevron deference add complexity to the litigation environment. Nevertheless, companies should begin actively preparing to meet the requirements of the final rules on the applicable timelines.

While the final rules represent a moderately scaled-back version of the proposed rules, the new disclosure obligations will nonetheless require significant and extensive preparation, and King & Spalding stands ready to help our clients address the nuances and complexities.