A Critical Link Between Insolvency and Rehabilitation

An otherwise viable business experiencing a cash flow crisis may seek relief under Chapter Four of the Kingdom of Saudi Arabia (“KSA”) Bankruptcy Law (“Bankruptcy Law”), a flexible statute that helps facilitate the financial reorganization of distressed commercial and individual debtors. These rehabilitative cases are known as Financial Restructuring Proceedings (“FRP”).

When a debtor runs out of cash before entering FRP, or when net cash flows are insufficient to keep the business running and pay the costs of the FRP, a debtor will need cash to survive until it can be rehabilitated through a court-approved restructuring plan. That is where the FRP lender comes in.

As of late 2022, debtors and lenders have not yet made extensive use of the Bankruptcy Law’s post-petition financing provisions. As a result, insolvent companies with cash needs but no other financing alternatives have resorted to piecemeal sales of assets to raise capital, they have liquidated, or they ended up being undercapitalized as they emerged from court supervision.

This article provides an overview of loans to a debtor after it has commenced its FRP case (“FRP Financing”), as well as the tactical uses to which such loans can be put to benefit the lender or debtor. International practitioners will find many of the same features and guiding principles that are embedded in United States and United Kingdom insolvency statutes. We first describe secured FRP Financing and the priority of security the FRP lender may hold, whether (a) in a FRP case that proceeds to an approved plan of reorganization, or (b) in a case that is converted to a liquidation under Bankruptcy Law Chapter Five. We then discuss the less common unsecured FRP Financing alternative and the priority it may hold. Next, we discuss exit financing provided to fund the debtor as it commences operations under an approved FRP reorganization plan. Finally, the article describes the strategic uses of FRP Financing, whether extended by pre-FRP lenders or opportunistic lenders.

FRP Financing: The Basics

- Secured FRP Financing

Bankruptcy Law provisions govern loans to a debtor after the commencement of a FRP case. A debtor must obtain approval of the bankruptcy court (i.e., commercial court) to obtain secured FRP Financing. In seeking such approval, the FRP debtor must attach to its court application an expert report supporting the request. The law provides, “The Court will approve the application when it is necessary for the continuation of the Debtor’s activities or for the protection of Bankruptcy Assets during the Procedure.”

The law does not provide specific criteria for approving terms of FRP Financing, and courts have wide discretion to determine whether to approve or reject a proposed loan. In jurisdictions where insolvency financing is common, debtors often seek competitive bids for the loan and select the best available terms to enhance the likelihood of Court approval.

Documentation for a FRP loan is virtually identical to that of a non-FRP loan, except that it will contain certain provisions specific to the FRP case. For instance, the loan agreement will include conditions precedent specifying that the loan must be approved by the court and must not be subject to any right of appeal to a higher authority. Maturity of a FRP loan will normally be shorter than a typical term or revolving loan, and termination events may include conditions the lender hopes to avoid in the course of the FRP case, discussed subsequently. Remedies will also need to take into account the existence and timing of any moratorium under Bankruptcy Law Article 46.

- Secured Financing (Non-Priming)

FRP Financing may be secured by a pledge of an unencumbered asset, or a pledge of a junior security interest in an encumbered asset. This sort of financing is similar to non-insolvency financing; it requires an economic assessment of the collateral value to ensure that the lender is fully protected, as well as other traditional underwriting analysis.

- Secured Financing (Priming)

In addition to junior secured financing or financing secured by unencumbered property, a FRP loan may hold a higher rank than existing liens if the court determines that the rights of current lenders will not be affected. A priming security interest can only be approved if (a) the value of the collateral is sufficiently high that a priming lien will not threaten other lenders looking to the same collateral, and (b) the debtor protects existing secured creditors from diminution of the value of the collateral.

- Priority of Secured FRP Financing

Priority of FRP Financing When a Plan is Confirmed

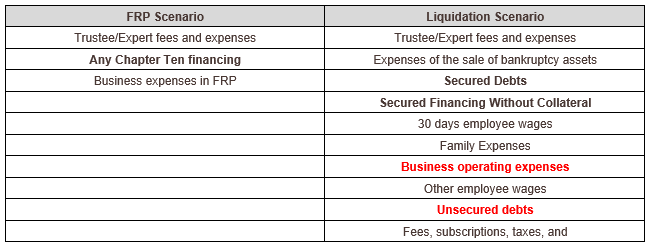

Because the Bankruptcy Law prohibits a reorganization plan from contravening the ranking of debts, the Bankruptcy Law and Implementing Regulations effectively prescribe the priority of payments in a FRP plan. In a FRP case, the top three levels of priority are as follows: trustee and expert fees rank first; FRP Financing ranks second; and expenses for the continuation of the debtor’s business, including trade and employment expenses, rank third.

FRP Financing Where the FRP Converts to a Liquidation Case

If a FRP case were converted to a liquidation case, then expenses of the estate—primarily trustee fees/expenses, expert fees/expenses, and expenses of the sale of the debtor’s assets—rank above all other debts (including FRP Financing), and must be satisfied prior to the further distribution of sale proceeds of the debtor’s assets.

After such trustee and sale expenses, secured debts (with security in rem) lie at the top of the waterfall. These are followed by (i) financing that asserts priority over unsecured claims but is not secured by a junior or priming lien on assets, (ii) thirty days’ worth of employee wages, (iii) family expenses pursuant to a regulation or court order, (iv) business operating expenses, (v) prior employee wages, (vi) unsecured debts, and (vii) fees, subscriptions, taxes and government entitlements.

- Unsecured FRP Financing

Unsecured financing may be obtained without court approval, so long as the debtor obtains the approval of the bankruptcy trustee. Where a debtor’s assets are fully encumbered by liens, unsecured financing is not usually an attractive option except as a last resort and where there is a firm belief that asset values will rebound in the foreseeable future. Unsecured financing may also be obtained with a court order. In that situation, as described in the next section, the priority of repayment, in certain circumstances, may be better than unsecured financing without a court order.

- Priority of Unsecured FRP Financing

In a FRP case, the priority of court-approved unsecured financing should fall behind trustee and expert fees/expenses, but ahead of the costs of continuation of the debtor’s business, unsecured claims and distributions to equity interest holders. If the debtor’s FRP case converts to a liquidation, then unsecured FRP Financing without court approval would rank pari passu with other unsecured debt and behind the costs of continuation the debtor’s business. Under certain conditions, unsecured FRP financing with court approval would hold a priority immediately behind secured debts and ahead of employee wages and business expenses.

The following chart comparing debt rankings in a FRP case and in a liquidation scenario shows where court-approved secured and unsecured FRP financing rank (in bold). Unapproved unsecured financing, by contrast (in red), can rank as a business operating expense or at the same level of unsecured debt:

Exit Financing

When financing is used to enable the debtor to emerge from the FRP process, it is often called “Exit Financing.” Exit Financing often looks more like a long-term business loan, because it is designed to fund operations after emergence from FRP as a profitable enterprise. Frequently, a component of exit financing pays off the short-term FRP Financing. Exit Financing is typically a component of a court-approved restructuring plan, and terms or detailed documents may be set out in the plan.

Strategic Uses of FRP Financing

A FRP loan can confer advantages upon the lender by providing opportunities to shore up collateral and minimize vulnerabilities. Where a debtor is faced with the prospect of shutting down and liquidating in the absence of a loan, the lender enjoys leverage that it may not have held prior to the filing of the FRP case. In addition to preserving collateral value and profiting from accrued commissions and fees, FRP Financing may enable a lender to negotiate more favorable covenants reflecting the current lending environment; set milestones for the progression of the FRP; fund litigation; or roll the old loan and FRP facility into one clean package.

Opportunistic FRP Financing

In some cases, the lender may not have a pre-FRP relationship with the debtor. Where a debtor has sufficient equity in its assets (for instance, in older “name” loans based on guarantor liabilities rather than collateral value), a “stranger” may extend the loan as a means of deploying capital with a favorable rate of return. The opportunistic lender will naturally want to ensure it is appropriately protected, as with any loan.

Conclusion

As the Bankruptcy Law matures, debtors will confront courts with increasingly complex business scenarios requiring creativity within the bounds of the law. Fortunately, the Bankruptcy Law provides a number of options for an opportunistic or relationship lender to aid the debtor’s rehabilitation through timely capital infusion. As practitioners, lenders and courts grow in experience and sophistication, FRP Financing is poised to become a prominent tool to assist in rehabilitation of insolvent Saudi enterprises.